If you have coerced debt, then you are a victim of identity theft. You have the same protections and remedies as victims of identity theft whose identities have been used by strangers.

As a victim of identity theft, one of your most important rights is that you can have fraudulent debts blocked from your credit reports. This means that people or businesses who check your credit reports won’t see the fraudulent debt. You may also be able to successfully dispute your responsibility to pay the debt.

Texas’ identity theft protections include protections for victims of coerced debt—where an abuser takes out debt in the name of a victim or where a victim of abuse is forced or threatened by an abuser to take out debt. The law is designed to protect victims of domestic abuse from this type of financial abuse.

The Fair Credit Reporting Act is one of the laws that deals with the rights of identity theft victims. If you are the victim of identity theft, you have a right to:

- Block fraudulent information from your credit reports and be notified if a block is declined or later removed;

- Stop creditors and debt collectors from reporting fraudulent accounts to credit bureaus;

- Dispute fraudulent or inaccurate items on your credit reports; and

- Get a response to your claim of identity theft.

- Place a 7-year extended fraud alert on your credit reports by providing an identity theft report (see Guide 2); and

- Get two free copies of your credit reports from each of the consumer reporting agencies when you have an extended fraud alert in place (in addition to the free annual copy available to everyone).

Tip: Any person who wishes, including victims of identity theft, can place a credit freeze on a consumer report, as a protection from any new, unauthorized credit accounts. Guide 2 has details on what to do.

If you suspect that you are or might become a victim of identity theft, you can have a one-year initial fraud alert placed on your credit reports (see Guide 2).

None of these things happen automatically. And while you can do many of these things yourself, it is helpful to have an attorney work with you.

Our List of Domestic Abuse and Legal Resources has a list of free and low-cost legal services.

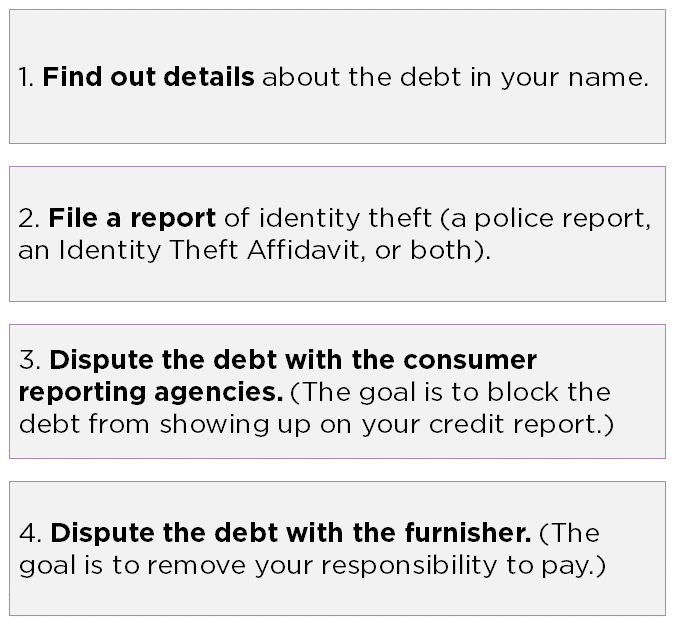

Steps for Disputing Coerced Debt

Texas passed a new law in 2019 expanding the definition of identity theft.

The new definition clearly covers coerced debt where the victim consented to the debt because of threats, force or fraud.

This new law went into effect on September 1, 2019 and applies to coerced debt transactions that take place after that date.

It is important to note that coerced debts where the victim did not consent to the debts are already covered under previous law, and so it does not matter when that debt was taken out. It is considered fraud and qualifies as identity theft.

Texas law also has long included a criminal violation for credit card abuse, where the credit card of a victim is used with coerced consent—consent induced by force, threat, or fraud. If you are a victim of coerced debts related to credit card charges, you may be able to get protections as a victim of credit card abuse.

See Tex. Penal Code §32.31(b)(1)(A) and §32.51(b)(1).